The Brexit referendum in 2016 was marked by claim and counter-claim on the impact leaving the European Union would have on trade between the UK and the 27 remaining nations. This was a major channel by which Brexit was expected to reduce national income: by erecting trade barriers and reducing trade volumes, leaving the EU was expected to discourage would-be exporters from investing in the UK, and by sheltering domestic producers from the bracing winds of international competition, Brexit reduces the incentives to invest and innovate. Yet it’s only now that we’ve left the single market that these claims can begin to be put to the test.

Monthly trade figures published in March showed that total trade (that is, imports plus exports) with the EU-27 fell by a third in January compared to the previous month. New figures released today show a partial bounceback, but trade with the EU-27 remains well below 2020 levels. But exiting the single market at the same time that a new wave of Covid-19 was hitting the UK makes this an unreliable estimate of the impact of Brexit alone: it’s likely that trade would have fallen in January anyway as the UK began another lockdown. And there may have been some stockpiling of goods in December as traders anticipated disruption in the New Year, especially as it was unclear whether the UK would secure a trade deal until very late in the day.

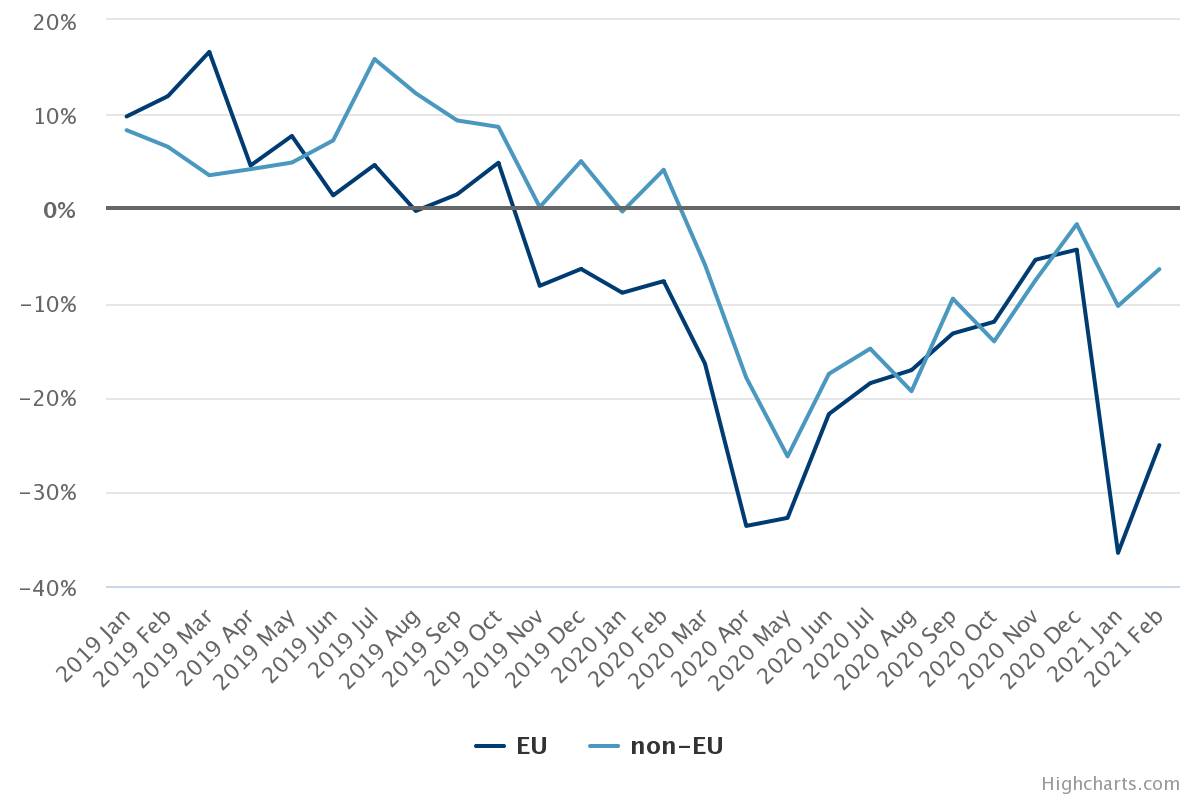

Another approach, then, would be to compare changes in trade with the EU-27 with changes in non-EU trade. Both will have been affected by the pandemic, but only EU trade is affected by Brexit. Comparing EU and non-EU trade in goods to its level in the same month two years previously[1] shows that whereas non-EU trade was 10 per cent lower, EU trade was 36 per cent lower than it had been in January 2019. Similarly, in February EU trade was 25 per cent lower than in the same month two years previously but non-EU trade was only 6 per cent lower. Interestingly, looking back earlier in 2020 shows that both EU and non-EU trade were a similar amount lower relative in the summer and autumn, suggesting that the pandemic reduced EU and non-EU trade roughly equally. The 26 per cent difference between the falls in EU and non-EU trade in January and 19 per cent difference in February can therefore be attributed to Brexit.

Change in total trade excluding precious metals on two years previously

Source: TBI analysis of ONS trade statistics

How does this compare with other estimates? Analysis by the Centre for European Reform suggests that single market exit reduced total UK trade (that is, with both the EU-27 and the rest of the world) by 22 per cent in January. By contrast, given that just over half of the UK’s trade is with the EU-27, our estimate corresponds to a 10–14 per cent reduction in total trade. Their estimate involves comparing actual UK trade with that of a ‘doppelgänger’ UK created from a weighted average of other countries (the largest contributors to the doppelgänger are the US, Germany and Canada) selected to match import and export trends in the prior period. It’s possible that a reason behind their larger estimate is that other countries that form part of the doppelgänger were less badly affected by Covid at the start of 2021: the UK had a higher rate of cases than these three countries for most of January and had the most stringent lockdown. An interesting contrast between the two estimates is that the ‘doppelgänger UK’s’ trade increased month on month in January, whereas the actual UK’s trade with the rest of the world fell by 6 per cent. Unless Brexit also reduced trade with the rest of the world, it’s hard to see why we would have expected trade to rise in January if the UK hadn’t left the single market. This suggests that the doppelgänger approach that relies on data from other countries that were not as badly affected by Covid may be overestimating the impact of Brexit.

Interestingly, our estimate is closer in line with estimates of the long-term impact of Brexit on trade made before the referendum by the much-derided experts, widely panned as part of ‘Project Fear’ by Brexiteers. The OECD estimated that Brexit would reduce UK trade by between 10 per cent and 20 per cent, NIESR’s estimate was between 15 per cent and 19 per cent in the immediate aftermath of exit with a trade agreement, the LSE’s 12.6 per cent in a similar scenario and the much-maligned Treasury estimates were for a drop of between 14 per cent and 19 per cent.

Of course, it’s still early days. It will take months or even years for the longer-term effect of Brexit to become clear. As traders get used to the new arrangements for trade with the EU-27, trade may continue to pick up – though a change in the way the ONS collects trade data will also have depressed the January figures and boosted the February ones – or some existing traders may decide to stop trading due to the new procedures. And there is still potential for trade deals with non-EU countries to partially offset the reduction in trade with the EU-27. For the moment, though – and not for the first time in the Brexit process – it looks as though Project Fear has become Project Fact.

[1] We use a two-year window as trade at the end of 2019 was similarly affected by uncertainty over the EU withdrawal agreement making the year-on-year difference affected by Brexit at both ends). We also exclude trade in precious metals which can be volatile.