Chapter 1

Today, the internet is the beating heart of the world. And just as the roads, railways and canals provided the arteries for commerce in the Industrial Revolution, today’s network infrastructure is the circulatory system on which much of modern life depends. Without it, the ramifications of Covid-19 would have been far more severe.

That we have been able to use the internet to mitigate the impact of the pandemic is a small relief, but the Covid-19 crisis has emphasised the importance of everyone being connected in the future. Eradicating extreme poverty, solving the global education crisis, building better health-care systems and responding to pandemics effectively all require connectivity. For low-income countries, being largely excluded from the exponential potential of the internet means that they cannot transform their nations. It is extraordinary that today half the world remains offline.

Closing the digital divide by 2030 should be one of the primary global policy priorities. Accelerating internet expansion will drive economic growth and enable progress and – as this report from my Institute demonstrates – the benefits of investment vastly offset the costs. It outlines the urgent action required on stimulating demand, regulatory reform and greater global coordination, and how a new digital coalition needs to be formed to transform opportunity and access for billions of people.

But prioritising internet access is not only about poverty alleviation. During these past years of isolationist and unilateralist policymaking by Western governments, China has been taking a more dominant role in developing economies. It has been investing in digital hardware infrastructure, taking an active role within international bodies and influencing the standards and values that underpin the internet.

This requires strong global leadership. Collaborating with China, as well as competing. Stewarding the right global coalitions around investment to achieve universal internet access. Leadership with the vision, commitment and confidence to establish the internet for a prosperous and inclusive global society.

We’ve lost our way on this in recent years, but an open and connected world will be the lifeblood for our future growth. It’s time that we make it a reality.

Tony Blair

Executive Chairman

Chapter 2

The Covid-19 pandemic has thrown out the usual playbook for economies, societies, businesses and governments around the world, and, in the process, it has accelerated the transformation to digital by as many as ten years. This shift has underscored the imperative to embrace and cultivate digital transformation across all industries, and in doing so, it has shone a stark light on the plight of the unconnected.

While great strides have been made to promote connectivity on a global scale, 46 per cent of the world’s population still does not have access to broadband connectivity. The pandemic has been a reality check for those countries and economies slow to adopt a strategy to connect the unconnected.

Access to education, improving health care, building sustainable cities, achieving gender equality, delivering clean energy, driving economic growth and eliminating poverty all require access to digital services and technology. Nearly every aspect of the UN’s Sustainable Development Goals and the revitalisation of the global economy depends upon access to broadband connectivity, the internet and digital platforms.

Health, education, governance and commerce have all made a dramatic shift to online platforms and applications. Digital interaction has become the de facto mechanism for families, communities and corporations to connect, communicate and collaborate.

Connectivity has become a necessity, and to lack connectivity is to lack the ability to fully participate in society and the economy.

In India, Reliance Jio was the first to offer free voice and affordable 4G data, fundamentally disrupting the digital divide and providing the ability for all to connect to the internet. Using this approach, Jio has led the digital transition, enabling all Indians to realise the full benefits of access to health information, public services and citizen services, including digital payments and ecommerce. New technologies are helping to reduce pollution, improve resilience to climate change and increase energy efficiency. With access to broadband, the new digital economy has accelerated adoption of several socioeconomic platforms, including proliferation of the India Digital Stack of Aadhar (Universal Identity) and the Unified Payments Interface (UPI), and it has had a significant impact on the way people live and work.

It is Jio’s relentless drive to connect all of India to broadband. This is an essential and crucial first step to ensure full participation in and access to the new digital society. Universal access is critical to uplifting everyone across all income levels. The ability to access the internet provides a truly level playing field and a clear and sustainable path towards long-term economic and societal growth. By designing and developing the most affordable 4G phone in the world, the highly intuitive Jio Phone has been instrumental in providing universal access to the internet.

Since day one, Jio’s guiding principle has been to provide affordable, high-quality broadband to meet the inherent demand among the unconnected across India. To effect change, we fundamentally transformed and disrupted business and service models, creating and using new technology and processes that addressed the aspirations of all of India.

Just four years ago, Jio was deployed as a green field, all-IP, all-4G Pan India network to ensure the greatest broadband reach. We invested in technology and talent development. We implemented an extensive fibre network and created a suite of applications, affordable devices, energy-efficient towers and sites, and meaningful digital platforms and services. Today, Jio reaches over 99 per cent of India’s 1.4 billion population and has over 400 million users.

Global collaboration and a coordinated effort consisting of public and private investors is imperative to accelerate connectivity in those countries still lacking broadband. Capturing the gains of the digital economy will require streamlining regulations, making it easier for startups to launch and scale, as well as introducing policies to facilitate retraining and new economy jobs for workers.

Funding for digital initiatives must increase, as should policies that drive innovation and investment that equalises access to and the availability of digital connectivity and services of meaning to all people. While some organisations and governments may rethink their digital transformation as the economy has slowed due to Covid-19, it is essential that we instead use this time to expand and grow connectivity so that no one is left behind.

All stakeholders need to respond effectively if the unconnected regions are to achieve their digital potential. Businesses must anticipate the digital future and invest in building capabilities, including partnering with universities and cultivating talent to deliver digital projects. Governments will need to invest in digital infrastructure and public data that organisations can leverage, all while putting in place strong privacy and security safeguards.

The quantum leap in digital acceleration has driven significant change in the daily life of consumers, businesses and government, highlighting the importance and value of technology. We cannot fail to capitalise on this opportunity to bring access and, more importantly, value to all.

Mathew Oommen

President, Reliance Jio

Chapter 3

The internet is a fundamental part of daily life. The connectivity it provides underpins social and economic interactions in the 21st century. This has been brought into sharp relief by the pandemic as many of us have migrated online to continue to work, to learn, to stay in touch, to buy food to eat. Yet half of the world remains cut off from these opportunities.

The world is blighted by a digital divide. In total, 3.7 billion people have no internet access. The majority are in low- or middle-income countries (LMICs). In the developed world, just 13 per cent of people lack a connection compared with 53 per cent in developing nations, and 81 per cent in the least developed countries. Along with the country a person lives in, gender is also a factor: Globally, women are 23 per cent less likely than men to use mobile internet.

The digital divide matters because it stands squarely in the way of progress. For LMICs seeking to transform their economies, it is increasingly the case that they cannot do so without the internet. Likewise, internet access is essential in efforts to eradicate poverty, improve education and build effective health-care systems, and it has a significant role to play in responding to crises like the Covid-19 pandemic. (The Tony Blair Institute, for instance, has partnered with Oracle to deliver a cloud-based Health Management System – launching initially in Ghana and Rwanda – to help countries manage essential vaccination programmes by creating an electronic health record.)

The potential benefits of universal internet access far outweigh the costs of achieving it. The returns to GDP alone for LMICs are vast compared to the investment that would be necessary to bring everyone online. And there are wider socioeconomic benefits that internet access affords. These include improved health and education outcomes, and potential redress of gender inequalities through financial inclusion. This is particularly true if internet access is rolled out as a central feature of countries’ socioeconomic development plans, working together, for instance, with their agro-industrialisation strategies.

But expanding internet access doesn’t only help to alleviate poverty and develop entire nations. A better-connected world benefits all countries, and building an open internet based on liberal values should be a foreign policy priority.

China’s influence on internet access in LMICs presents serious geopolitical and security challenges including cybersecurity and the fact that social media is a critical source of information for intelligence services today. Developing countries are highly unlikely to shift away from the use of China’s technology in this space, so Western democracies and other democratic countries such as South Korea and Japan need to collaborate with China as well as compete. The imperative must be to build an open and inclusive internet infrastructure that is premised on human dignity, liberty and freedom, enabling all people to forge their own opportunities to learn, to innovate and to thrive. Creating a universally accessible internet based on these liberal values should be a key area of cooperation for the Biden administration and European leaders as they re-establish the transatlantic alliance.

Closing the Digital Divide as a Global Policy Priority

There are several global initiatives and coalitions focused on addressing digital inequality, and progress is being made – but as yet there has not been the political leadership to drive this agenda forward with the urgency required. The Biden administration could well provide the leadership that this critical challenge requires. If the United States and other liberal democracies hope to lead the world in the 21st century, they must ensure that global access to information is protected. If China can cement its digital infrastructure throughout the developing world, it not only diminishes the influence of the United States and other liberal democratic countries abroad but could also lead to national security risks further down the road.

We estimate – drawing on existing analysis – that the investment necessary to close the digital divide by 2030 is approximately $450 billion. To put this cost in perspective, raising these funds would require member countries of the Development Assistance Committee – an arm of the Organisation for Economic Cooperation and Development (OECD) – to contribute 0.02 per cent of their gross national income (GNI) per year. That is the equivalent of just 3 per cent of the 0.7 per cent overseas development assistance (ODA) aid target set by the UN and which the UK once adhered to – a small price to pay for a foundational investment that would enable low- and middle-income countries to forge their own paths to prosperity.

But this is not just about investment. Closing the digital divide requires a roadmap to detail how universal internet access can be achieved by 2030. Based on our analysis, we propose three key policy recommendations.

First, a coordinated effort to stimulate demand for 4G or equivalent broadband technologies, to make more infrastructure investments viable.

The private sector can and should provide investment to expand 4G or equivalent broadband coverage, but it needs a market to drive that demand. Public investment of approximately $58 billion to increase smartphone access, build digital skills and improve internet content to make it relevant to those offline will go some way towards building up that demand for 4G or equivalent broadband networks, and could help lay the foundations for 5G in the near future.

Regional coordination, such as that currently exhibited by Smart Africa, can drive down the costs associated with accessing the internet – data and smartphones – that prohibit much of the developing world from coming online now.

It is essential that efforts to address the digital divide are situated as part of the emerging industrialisation plans of many LMICs. Efforts to transform entire economies so that jobs can be created and household incomes expanded across countries are key to stimulating demand. The connection between digitalisation and industrialisation is multifaceted and is one that merits further analysis in future research.

Second, regulatory and policy reforms to open up markets and drive down prices for consumers.

Regulatory changes will be essential in closing the digital divide. These must aim to both increase ICT market competition and also reduce taxes on basic smartphones and data that currently contribute to access being prohibitively expensive. National broadband plans will be critical to ensure public investments are more effective and are coordinated with private investment.

Some administrations in LMICs may find it politically difficult to take the right policy steps to drive universal internet access. Donor countries can support leaders to make the politically or indeed fiscally challenging policy changes now, in order to reap the benefits of universal internet access in the medium term.

Third, global coordination to diversify and expand investment vehicles for 4G or equivalent broadband coverage.

More than 85 per cent of the investment required will need to address 4G or equivalent broadband network expansion and maintenance. It is anticipated that the private sector can and should meet 75 per cent of this investment, with public investment focusing on the most commercially unviable investments. But the current market for 4G or equivalent broadband network expansion is not fit for purpose. Universal 4G or equivalent coverage needs to be facilitated by boosts to demand from public investment and national regulatory change, as well as global coordination to diversify the range of investment vehicles available to make it commercially viable.

Fixing this requires an investment coalition of institutional and global investors to increase the risk appetite and diversify the funds and vehicle structures available to meet the demand for 4G or equivalent broadband networks. It will also require political capital and capacity to coordinate with governments’ existing infrastructure works to ensure 4G or equivalent broadband expansion is achieved at marginal cost.

The Political Moment

Making faster progress on universal internet access will take determined geopolitical leadership. This should be a key agenda item for the G20 taking place in Rome in October 2021. The Italian presidency has made it a priority. As Prime Minister Mario Draghi looks to re-establish the transatlantic alliance, this could be a key area of cooperation for the US and European nations.

As we have highlighted, closing the digital divide is not only about solving global poverty but also about a statement of values: freedom, inclusion and opportunity for all.

The Sustainable Development Goals were an urgent call in 2016 to all countries to solve the most pressing development challenges by 2030. If universal internet access is not achieved by then, the digital divide we see today will only intensify existing inequalities. Solving the digital divide now – with universal internet access built on liberal values – is fundamental to building a prosperous and inclusive global society for generations to come.

Chapter 4

Throughout the Covid-19 pandemic, internet access has been critical for the continuation of our ‘normal’ lives, including work, relationships and commerce. Increasingly, it is also where we engage with government and receive public services.

But half of the world is still not connected to the internet.

One of the most significant and lasting impacts of the pandemic will be the seismic transition from analogue to digital in every aspect of our lives. The opportunity cost for those who are still not online will only grow. The digital divide is already magnifying existing inequalities, and this will intensify as more elements of our work, and public and private lives, are facilitated by digital technologies.

The Time Is Now

Technology develops at an exponential rate, in a way that no other sector does. The rapid rate of technological change creates an ever-growing opportunity cost for countries that do not invest in the foundations for internet-enabled growth and transformation. If countries do not invest soon, this will hold back development across all sectors, from health care to education.

The pandemic has revealed the vast disparities presented by the digital divide. For example, 94 per cent of learners were forced online regardless of whether students had connectivity or safe access to the internet. The World Bank has estimated that, without remedial action, it expects a $10 trillion loss in future earnings for the generation of students subjected to pandemic-related school closures in 2020 and 2021. This is exacerbating the already acute crisis in education across much of the developing world, with leaders only now understanding how essential connectivity and technology will be to recouping lost education for students, and supporting the recovery of economies and societies as the pandemic eases.

This growing inequality in education is being replicated across the human development indicators, with devastating macroeconomic impacts; developing economies are expected to contract by 2.5 per cent, their weakest performance for at least 60 years. Up to 100 million people are thought to have been pushed into extreme poverty in 2020, erasing all progress made in the last five years to put an end to people living in these circumstances by 2030.

As many of us migrated online to continue our work, our studies, and our social and civic engagements, the vast majority of the developing world remained shut out. If they remain offline, with extremely limited access or with suboptimal connectivity (such as 2G or 3G), they will miss out on a devastating number of opportunities. Internet access would aid post-Covid-19 recovery and give people access to advanced technologies which could help them overcome everyday challenges – for example personalised and adaptive learning software or AI-powered health detection and management applications. Universal internet access is pivotal to a leapfrog model of transformational development, enabling countries to bypass traditional stages of development to either jump directly to the latest technologies or explore an alternative path of technological development involving emerging technologies that offer new benefits and opportunities.

The Sustainable Development Goal target 9c aimed to provide universal and affordable access to the internet in the least-developed countries by 2020. This ambitious target has already been missed. Given its deadline coincided with the year that Covid-19 ravaged the world, this should mark the moment where we meaningfully galvanise support to reach this goal within the decade.

This is in all of our interests. Connecting the world will create new channels for the interchange of knowledge and information, adding to our collective understanding and creating new ideas. It will provide new economic activity and opportunity. It is a technological grand challenge and ambitious common goal that we should work towards solving today. This will require new digital coalitions for change which, as worries about the implications of a “splinternet” (or a divided internet, controlled and regulated by different countries) continue to increase, should commit to the principles of open technologies and standards. The splinternet is no longer just a concept; it is now a reality. This presents profound geopolitical and security challenges, including cybersecurity. Social media, for example, is a critical source of information for intelligence services today.

There are also strong economic reasons for investing in expanding internet access. The half of the world’s population that is currently unconnected represents a significant market opportunity. The Chinese government and Chinese companies are investing heavily in LMICs in Africa and elsewhere. The West must be able to match China and others on this front.

This agenda should be a priority for the Biden administration and the European Union, but it cannot be unilateral. It should be about wider re-engagement with countries committed to the same values. For those who believe in an open and interconnected world and want strong national security and economic prosperity in the 21st century, creating internet-era infrastructure for all should be a key concern.

Defining the Digital Divide

Forty-six per cent of the world’s population does not have access to 4G. This is in part driven by a lack of 4G coverage, but the reasons for limited uptake extend beyond this.

4G coverage of population by region, 2019

Source: ITU Connecting Humanity, 2020. Estimates based on GSMA, Xalam, UN population data.

In sub-Saharan Africa, for example, only 10 per cent of the population is using 4G, although half of the population is covered by a 4G signal. The majority of those not accessing the internet are either unable to afford it, do not know how to or do not see the utility in doing so, as opposed to not having an internet signal.

Closing the digital divide involves more than just providing broadband coverage. There are a variety of reasons why people do not access the internet. In 2018, the global telecommunications industry body the GSMA conducted a survey across low- and middle-income countries in key regions to illustrate the leading barriers to accessing the internet:

The top barriers to mobile internet use in surveyed low- and middle-income countries, by region, 2018

Source: GSMA Intelligence Consumer Survey 2018. Note: Data based on the single most important barrier to using mobile internet identified by mobile users who are aware of mobile internet but do not use it, averaged across surveyed markets.

Affordability, literacy and digital skills, and a lack of content that is locally relevant are usually cited as the most significant barriers to access according to the GSMA survey. These reasons were ranked higher, in fact, than access to a network. There are also some specific hurdles to overcome on a regional level. Perceived and actual safety and security online, for example, presented a great barrier for many in Latin America, but far less so in South Asia.

Another barrier highlighted, “family does not approve”, alludes to gender and other cultural factors that prohibit, or at least dissuade, the use of the internet by certain groups. The proportion of women globally using the internet is 48 per cent as compared to 58 per cent of men, and this digital gender gap is growing in developed countries. Digital exclusion is also amplified across social and cultural lines, affecting migrants, refugees, internally displaced persons, older people, young people, children, people with disabilities, rural populations and indigenous peoples.

For the purpose of this report, we identify the following four barriers as the leading issues preventing universal internet access:

Access to affordable data. A universal benchmark advocated by the Alliance for Affordable Internet (A4AI) defines affordability as “1 for 2”: where 1GB of mobile broadband data is priced at 2 per cent or less of average monthly income.[_]

Access to an affordable 4G-compatible device. This is predominantly a smartphone[_] but can include any 4G-compatible device capable of running 4G-powered applications (e.g., MiFi or a 4G dongle, but not a feature phone).[_] There is currently no global metric for what constitutes “affordability” but drawing on the affordability metrics for data should offer a meaningful comparator.

Digital skills and relevant content. This means the literacy and basic skills to not only access the internet itself, but the content available on it to make access a meaningful experience.[_] Content – including government-provided (such as government services), commercial and user-generated – needs to be locally relevant based on language and subject to provide an incentive to get online.

Coverage by a 4G or equivalent broadband network. Although 4G access was not cited as the leading barrier by some margin in the GSMA survey, it is nonetheless critical to transformational development. 4G and equivalent technologies (highlighted in Annex C) will enable advanced applications to be developed and used, with the potential for leapfrogging. Many basic online activities which fuel productivity and prosperity rely on a 4G or equivalent connection, with enough bandwidth and low enough latency to watch videos without buffering, conduct video calls without delay and participate in activities in real time as if they were in the same room.

While online security and safety and horizontal inequalities are also significant barriers to access for large proportions of the developing world, we chose not to address these directly in our analysis. This is in keeping with much of the existing literature that identifies the above barriers as the primary roadblocks to access.[_]

Furthermore, increasing affordability, expanding digital skills and enhancing the relevance of internet content to meet the needs of citizens will begin to address some of the inequalities currently amplified in digital access.

Online security and safety concerns must be targeted as part of a holistic digital-skills curriculum. Children and adults alike should learn about responsible internet use and ethical engagement online, allowing them to build key 21st-century skills around critical thinking and problem solving in order to considerately engage with, sift and balance the wide range of views and information online.

The financial and political threats posed by cyber criminals, or even governments themselves, are risks that are beyond the scope of this report. Policymakers liaising with law enforcement will need to build up credible mechanisms to protect users from cyber criminality and will need to draw on regional and international cooperation to do so. The risk that authoritarian-leaning governments may use internet access as an instrument of political control and deterrence is in some cases a very real threat, but it is one that should be met with meaningful engagement and not be used as an excuse to deny internet access to the citizens of those countries. Political suppression through internet use remains part of the wider geopolitical case for the Global North to influence the values around which, and therefore the mode with which, internet access is expanded.

Chapter 5

Internet Access Accelerates Development

Universal internet access will underpin the achievement of all the Sustainable Development Goals (SDGs) – from the human development ambitions set out in Quality Education (SDG4) and Gender Equality (SDG5), to economic growth through the Industry, Innovation and Infrastructure (SDG9) targets.

Increasing internet penetration has a significant macroeconomic impact: In low-income countries, a 10 per cent increase in mobile broadband penetration yields a 2 per cent increase in GDP; and, for middle-income countries, a 10 per cent increase in both mobile and fixed broadband penetration yields a 1.8 per cent and 0.5 per cent increase in GDP respectively. For low-income countries that continue on the trajectory towards middle income, increases in fixed broadband penetration will have a further positive impact on their economies.

But the effects of universal internet access are not just felt in productivity gains. It can also transform millions – indeed billions – of lives. The arrival of fast internet in Africa, for example, has yielded an estimated increase of between 6.9 and 13.2 per cent in jobs, regardless of education level. And this statistic does not just represent the formalisation of existing jobs, but the creation of new and better-quality jobs that are aligned with SDG8 (Decent Work and Economic Growth), with fewer workers holding jobs in unskilled occupations when fast internet is available. Increasing internet penetration levels to 75 per cent of the population in all developing countries is estimated to create more than 140 million jobs around the world.

Increased internet access is and will be transformational for individual sectors and industries, too, as seen in the wider economic transformation experienced by China and the “Asian miracles” in the second half of the last century. This is often considered the holy grail of development policy: the transformation of a low-productivity, agricultural-based economy into an advanced, highly industrialised one. To achieve this, developing countries must reach 21st-century levels of digital access and technologies in order to compete globally. For example, increased access to mobile phones and the internet for farmers reduces the price of inputs and asymmetries in information, and provides real-time data (such as accurate weather forecasts) alongside better advice on agriculture practices and inputs. This allows farmers in the developing world to compete more favourably with their global competitors. Universal internet access also paves the way for more advanced AgTech, which has the potential to revolutionise the industry. This will be critical for economic transformation, addressing poverty (SDG1) and improving food security (SDG2).

Universal internet access will significantly address global inequality and inclusivity, specific to SDG10 (Reduced Inequalities) but important to all the goals. It is estimated that there are 1.7 billion “unbanked” people in the world – i.e., those without access to traditional financial services – who would benefit from fintech by sending and receiving payments within and across borders, and accessing credit in ways that analogue methods of identification do not permit. Moreover, fintech and e-commerce promise to address the stark gender inequalities (SDG5) prevalent in financial inclusion. Digital financial services are expanding opportunities for women, increasing their engagement in the formal economy and strengthening their resilience to financial, economic and health shocks. The e-commerce revolution is reshaping the global business environment to provide more opportunity for small businesses, especially those headed by women.

Returning to education, internet access not only increases access to learning, but also can improve educational outcomes. Connecting every school would make a vast array of content available to teachers and students, and empower learners to build their confidence online and develop their own discipline of knowledge-seeking. In addition, rapidly evolving advanced technology such as EdTech applications are becoming more adaptive and responsive to individual learners’ needs, which could help bridge both the shortfall of approximately 69 million teachers by 2030 and the current global learning crisis in accessing quality education (SDG4).

The role of big data – premised on widespread mobile broadband penetration – and digitised health systems in supporting epidemic preparedness and response was well documented prior to Covid-19, and will now become integral to vaccine rollout and future pandemic-preparedness strategies. Digital health innovation will also be instrumental in addressing non-communicable diseases, which account for 70 per cent of deaths worldwide (three-quarters of which occur in the developing world). And advanced technologies such as AI could begin to address the acute deficit of 18 million health-care professionals anticipated by 2030 through many promising widespread innovations in clinical care pathways (prognoses and diagnoses); patient-facing solutions, such as personalised health advice and information provision; and far-reaching efficiencies in areas like health-systems management, drug discovery and clinical-trial design.

Furthermore, the transition to digital public-service delivery more broadly will yield many benefits, from cost savings and efficiencies to greater civic engagement. In the medium term this will outweigh the cost of transitioning from an analogue to digital model of government engagement, bringing related improvements to governance and transparency in public transactions too. Over time, these financial savings will likely outweigh the investments made to provide online access to all. An example of the vast progress that digital solutions can deliver for public-service delivery is the Copenhagen Consensus’s advice to the government of Bangladesh on prioritising development funding. Two digital solutions were recommended to bolster the delivery of public services: first, moving to an “e-procurement” platform to lower the costs and corruption association with the current outdated system; and, second, digitising the land-records system to deliver greater transparency and efficiencies.

Digital identification, or digital ID, is a primary example of how securing universal internet access can provide opportunities for significant returns on investment, contributing to the overall sustainability of efforts to close the digital divide. A secure, well-designed digital ID system can provide countries with a cross-sector platform that enables them to leapfrog to more efficient and modern systems, thus enhancing service delivery. Beyond developmental uses, digital identity promises to generate significant savings. Potential fiscal benefits include reducing fraud and inclusion errors in government-to-person transfers; lowering administrative costs; increasing tax collection; stimulating sales of goods and services; and improving labour productivity. Digital ID can therefore deliver significant economic value for the public sector, particularly in developing countries.

This is already being realised in some countries. In Botswana, biometric enrolment of pensions and social grants achieved savings of 25 per cent by identifying duplicate records and deceased beneficiaries. Similarly, in Nigeria, biometric audits reduced the federal pension roll by 40 per cent. The government of India has reported estimated fiscal gains of more than INR 825 billion ($11.31 billion at current exchange rates) between 2013 and 2018 as a result of digital ID-enabled direct benefits transfers combined with reforms to beneficiary identification, and refined targeting of social programmes and subsidies. While the exact return on investment can be disputed, these savings are thought to be around nine times the cost of implementing Aadhaar, the digital-identity system used in India.[_] There is therefore clear evidence that the investment to achieve universal internet access – including subsidising access for those most marginalised in society – would be economically advantageous.

Covid-19 has had a catastrophic impact on human life with dire economic ramifications for countries of all development levels. Yet not all outcomes are negative. One of the lasting repercussions will be the accelerated transition from analogue to digital government. The arguments for digital ID and “government-as-a-platform” were being made well before Covid-19 but, in the coming months, these concepts will become ever more critical to vaccination rollouts, mass testing and real-time track-and-trace services in order for life and the economy to resume as quickly as possible. None of this is possible without internet access, and this pandemic has illustrated how fundamental digital public-service delivery and engagement will be to building resilience ahead of future health disasters.

These are just some of the ways in which increased internet access is and will be transformational for development. When a developing country faces challenges with food, water, electricity, sanitation and health, it may seem counterintuitive to prioritise the expansion of internet access. However, research shows that digital solutions to address these problems can often be the most transformative and cost-effective. For example, the Copenhagen Consensus analysed the investment opportunities that would best address the main binding constraints to growth and development in Bangladesh and Haiti. The researchers proposed two digital solutions among their top ten recommendations. In Haiti, one of these recommendations was increasing internet coverage to 50 per cent of the population.

Closing the Divide Benefits Everyone

Universal internet access should be a key component in the growth plans for every country. For developing countries, it should be a critical element in their economic transformation strategies – without it they will fall further and further behind in an increasingly connected and digital 21st century. For advanced countries, this means a drawing away from aid dependency: Closing the digital divide will be critical to poor countries’ self-sufficiency as it will lead to transformational development.

For donor countries, the benefits of investing in universal internet access are real and are not limited to eventual reductions in foreign aid. International trade flows have been shifting away from a concentration in Global North-to-North, and even South-to-North, trade. North-to-South trade flows are already equal to those between North-to-North, and demographic trends indicate that this shift will only grow. Already, middle-class populations in advanced economies represent only 25 per cent of the world’s middle-class population. Growth of this demographic in the Global South is booming and expected to increase at a rate of 6 per cent or more per year, compared with a more moderate growth rate of 0.5 to 1 per cent in the North.

China already hosts the largest middle-class consumption market segment in the world, and by 2030 it will be overtaken by India, which will also surpass the US. The larger markets in the Global South – Brazil, Mexico, Pakistan, Indonesia, Egypt, Nigeria and Vietnam – each already host middle-class populations of over 100 million. Not only do the middle classes in the South offer a huge growth opportunity for companies in the North, but their share of e-commerce growth as a percentage of all retail spending is growing significantly. The tide of trade, in part driven by globalisation and a rapidly digitalising world, is changing and these growth markets will be ignited by universal internet access.

Rich countries will depend on the Global South to sustain their own export-led growth. This trade evolution over the last 50 years, with production also shifting from rich countries to key markets in the East, has presented its own challenges to the Global North, including slower than expected labour-market adjustments for those whose jobs have been offshored. While governments in the Global North must invest significantly in their own readjustment policies to support those struggling labour groups, the growing markets in the Global South will be critical to the Global North’s future prosperity and resilience.

On a macro level, the case for free trade is still hugely compelling and, for those who believe in the power of information and an interconnected world, the opening up of new nodes of knowledge is therefore also about enlightened self-interest. The transformative potential of internet access can create new wealth avenues for millions of people, with an open internet and more users providing the foundation for more choice and innovation in the global market.

The Internet, Inclusion and Liberal Values

This belief in economic openness and the power of technology extends further into the values and priorities that the centre of politics should pursue today. Harnessing technology and navigating its impact are the key challenges of our age and yet, despite being decades into the digital revolution, many still underestimate the impact of the internet. It is completely transforming all elements of society and opening opportunities that were thought nearly impossible not long ago. Part of the failure to recognise the impact of the internet is our present inability to fully quantify its value creation, let alone understand the causal effects.

However, the evidence surrounds us: The superstar companies of the modern age have capitalised on the economies of scale and strong network effects provided by the internet. Many of the breakthroughs at the frontiers of science are only possible because of the power of software and AI today. And though Covid-19 has shut off huge amounts of human activity, that which remains is almost all online. For those without the internet, the knock-on consequences can be catastrophic.

This is true even where access is relatively high. For example, when France reopened schools in 2020, it was partly influenced by the fact that 500,000 low-income students could not access remote learning due to no internet access. Internet access has therefore become fundamental for anyone who cares about equality of opportunities. It is a platform for life, learning and livelihoods. The centrality of the internet to modern life is why a number of political institutions including the EU and the UN have made affordable access key commitments. Some leaders, like Rwandan President Paul Kagame, have made calls for universal access.

From a moral perspective, access to the internet is therefore about more than a right to information; it is a matter of human dignity and of improving quality of life. Nobody can control the circumstance of their birth, and where an opportunity exists to help those most in need, there is a compelling case for doing so. Generosity of spirit is not about the deserving and undeserving, and as politics in many countries focuses on “in” and “out” groups, there is a risk of missing the bigger picture.

In an interconnected world, the case for access extends well beyond the internet being a fundamental building block for modern life. It is about liberty and freedom in that it connects people and businesses to ideas and to markets, allowing greater incorporation of developing countries into the world’s economy, alongside the opening-up of new experiences and opportunities. It is not a Trojan horse that centralises power with government-to-government transfers. Conversely, it is, in many ways, key to decentralisation and democratisation of the world, empowering more individuals with autonomy and an increased ability to engage in entrepreneurship and trade.

There is also a strong geopolitical component of the push to connect the world. Concerns endure over values, power and governance and, more broadly, the international democratic order for the digital world. Action should be taken by a coalition of nations who are willing to act according to principles compatible with liberal democratic values. Global technology companies, in particular the big tech giants, also have a responsibility to uphold these principles when bringing the internet to new parts of the world.

China has a critical role to play. Its pursuit of technological dominance and control of the modern digital economy, including through the Digital Silk Road, includes a hardware push to connect countries, as well as an attempt to influence standards through its filling out of international bodies, including the International Telecommunication Union (ITU). As Sangeet Paul Choudary has written, such pursuits, along with other aspects including the smart cities push, form China’s “country-as-platform strategy for global influence.” The risk of a splinternet and a break in the internet’s shared and ubiquitous architecture would present profound geopolitical and security challenges, including cybersecurity and the fact that social media is a critical source of information for intelligence services today.

After years of more isolationist and unilateralist policy, democratic nations need to be more determined to collectively help build the infrastructure and standards of the digital highways that connect everyone in the world today. This should therefore be a key question for the Biden administration, whose China strategy needs to rise above the partisan rancour and be clear-eyed in its assessment, understanding that technology is central to the debate today and that competitive collaboration should define relations. Competition with China does not require confrontation.

There is almost certainly going to be a break from the Trump administration in this regard, who put significant stock on this question but whose proclamations veered towards indictments. Following Donald Trump’s failed bid for re-election, the State Department published a paper on The Elements of the China Challenge, which highlighted some of the key aspects that have concerned the US government. This included highlighting their view that “China aims to build the world’s fifth generation (5G) wireless-telecommunications physical and digital infrastructure as a steppingstone to broader dominance in emerging and next-generation information technologies”, which was central to Trump’s attempt to stifle Huawei. The UK took a similar stance, banning the installation of Huawei equipment on UK networks from September, although the company already has a strong foothold in Africa.

The company is active in South Africa’s network and is working with Safaricom in Kenya, while another Chinese company subject to US action, ZTE, is active in Uganda. Around 70 per cent of 4G base stations on the continent are made by Huawei, which already signed a contract for South Africa’s first commercial 5G network. The company is also involved in initiatives including the Smart Africa Alliance and A4AI alongside Google, Facebook and Microsoft.

Chinese companies are investing in new technologies which could connect the planet. Satellite technology is advancing, opening up potential new opportunities for connecting the world’s population through LEO (low Earth orbit) satellites (see Annex D). While US company SpaceX is the most advanced in its efforts with LEO satellites, the Chinese government is also investing in the technology. The Hongyun Project plans to launch 300 satellites into low Earth orbit, with the network operational in 2022 and complete by 2025. Chinese companies, usually in close coordination with the government, are also investing in LEO satellites. The Chinese firm LinkSure Network has announced plans for a constellation of 272 satellites with ambitions to provide free Wi-Fi to regions currently without coverage.

Developing countries are highly unlikely to shift away from the use of China’s technology in this space, which is why the US and other nations are going to have to put more weight behind this issue. This will require collaborating with China, as well as competing. The pursuit of an open internet should therefore be of key strategic interest for democratic nations, and these reasons feed into why they should put their investment in universal internet access.

President Biden has emphasised the integral role of ICT to the “summit of democracies” he will convene. Access to the internet and all it entails should be central to any new digital alliance of democracies. But the issue is wider than this: New forms of technological cooperation, which also include companies, are key to the transatlantic alliance; key to relationships with countries such as Japan, South Korea and Australia; and should advance individual rights and dignity, and democratic principles and values. But China’s increasing technological dominance means that it will be both pragmatic and necessary to collaborate with its government and companies on these issues in the coming years. It would be naive to believe that cooperation with liberal democratic nations will influence China’s values, but finding partnerships for development will be necessary for the balance of power in the decades to come.

Chapter 6

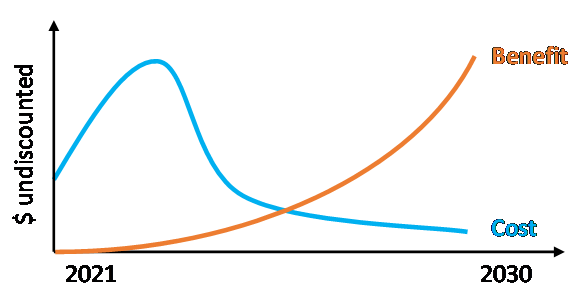

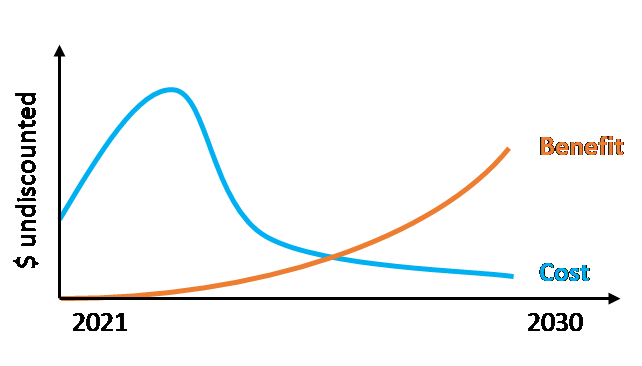

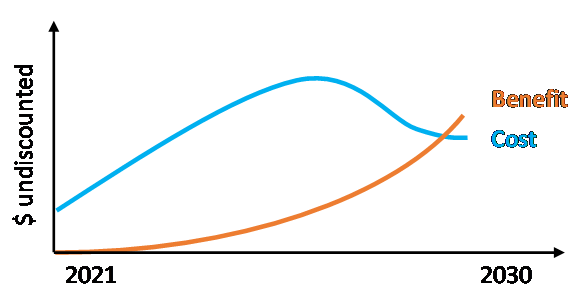

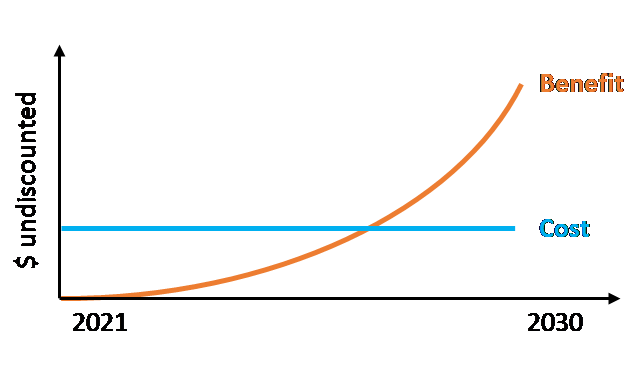

We estimate that it will cost in the region of $446 billion to achieve universal internet access by 2030 and that it could deliver $8.7 trillion in benefits to developing countries. The sequencing of the investments is a policy decision, and the benefits are likely to accrue with an uncertain time lag. We investigated a range of different scenarios for timing and discount rates. We found that in every case the benefits outweigh the costs.

The Scale of Investment Required

The ITU and A4AI, which do not include devices, estimate that it will cost approximately $428 billion to achieve universal internet access by 2030. We estimate the devices gap could be closed with an investment of $18 billion. This makes a total cost in the region of $446 billion to achieve universal internet access by 2030.

Investment needed to achieve universal access to broadband connectivity by 2030 (does not include devices). Total: $428 billion

Source: Estimates based on ITU, GSMA, A4AI, operator and regulator data. From ITU, 2020 Connecting Humanity.

The usage gap – driven by affordability, skills and internet relevance issues – is the greatest barrier to internet access (see Figures 1 and 2). Despite this, the bulk of investment needed to close the digital divide is for 4G or equivalent broadband infrastructure (89 per cent). This includes: mobile radio network capital expenditure (capex) for greenfield investments to expand 4G mobile coverage to underserved areas; upgrades to existing 2G and 3G networks; the installation of network backhaul infrastructure covering metro fibre, microwave or satellite; and continued network operations and maintenance costs through to 2030. The infrastructure investment includes a satellite/Wi-Fi requirement for remote areas which are out of reach of traditional mobile networks (between 10 and 20 per cent of the rural population in most countries) and localised solutions for coverage will be needed, consisting of satellite backhaul and fixed wireless access (predominantly Wi-Fi) for the last mile (these technologies are highlighted in Annex C). Innovative technologies to increase connectivity will no doubt emerge and develop between now and 2030. The potential of LEO Satellites to bring low-latency, high-speed connectivity to this demographic is particularly promising (discussed in Annex D).

This investment also includes $40 billion (9 per cent of total investment) for improving digital skills and enhancing relevant content for the internet to be meaningful. This, for example, could include access to content in local languages or information relevant to the day-to-day lives of the unconnected (e.g., pricing data for smallholder farmers).

$6 billion (1.4 per cent of total investment) is allocated to driving policy change to liberalise markets and increase competition in the sector, bringing down prices and encouraging network expansion.

The total estimated investment figure of $428 billion is based on a model that assumed the most cost-effective data network was available.

Below is the distribution of investments by region.

Investment requirements by region (does not include devices). Total: $428 billion

Notes: Country groups based on World Bank classification. This includes high-income countries, comprising 6 per cent of total investments.

Source: Xalam estimates based on ITU, GSMA, A4AI, operator and regulator data. From ITU, Connecting Humanity, 2020.

Factoring in the Cost of Devices

The ITU’s global costing model does not include the cost of devices. We estimate the devices gap could be closed with an investment of $18 billion. A4AI has undertaken a separate project evaluating the cost of devices across the developing world today. Of the large number of countries it evaluated, it established that the cheapest smartphone available was in Lesotho at $17.96 (2020).

By comparison, an initiative between Google and Safaricom in Kenya to expand 4G access offers a range of more affordable smartphones with repayment plans – common in the West but unusual in the developing world. Its “Neon Ray Pro”, for example, is a 4G Android (Go edition) smartphone retails at Ksh 6,500 ($58.83) and can be acquired with a downpayment of Ksh 1000 ($9.05), with the outstanding amount repaid over nine months at Ksh 20 a day ($0.18). Given a basic entry-level salary in Kenya is $5.00 per day, this makes device repayment 3.6 per cent of a modest lower-income salary. This is comparable to the universal target for data affordability (1GB at 2 per cent of monthly income).

We estimate that between now and 2030, an additional 837 million people will need assistance in accessing a device. Of those, around 385 million will still be living in extreme poverty (<$1.90 a day) and may, in the first instance, require subsidies to cover the full cost of a smartphone if they are to access the internet.[_] We assume that the remaining 453 million will be able to access a competitively priced device on a repayment plan, similar to the example offered now in Kenya.

Assuming the cheapest smartphone available today ($17.96) can be purchased at scale for those living in extreme poverty by 2030, and a device repayment plan similar to that offered by Google and Safaricom ($58.83) can be made available for the remaining 453 million not accessing the internet for affordability reasons, we estimate the devices gap could be closed with an investment of $18 billion.[_] This would include subsidies for the extreme poor and donor support to underwrite loan-guarantee schemes offered by telecoms companies to offer smartphones for the lowest-income groups. The $18 billion figure represents 4 per cent of the total investment outlined by the ITU.

Estimating the Economic Benefits

The direct economic benefits from universal internet access are significant. We estimate that the direct economic benefits from universal internet access to the developing world total approximately $8.7 trillion.

The ITU conducted a series of global and regional econometric modelling studies to estimate the impact of a 10 per cent increase in internet penetration on GDP, the results of which we summarise below:

Table 1 – Impact on GDP of a 10 per cent increase in mobile and fixed broadband penetration, by income group and region

We applied the ITU’s analysis to current GDP levels, modelled against expected population growth and aspirational internet access levels, to ascertain the impact of expanding broadband penetration to reach universal coverage by 2030.

Case Study

Key Definitions

Universal internet access: For the purpose of this report, we adopt the ITU and A4AI’s definition, which was developed by the UN Broadband Commission: Access to a 4G or equivalent internet connection for 90 per cent of the over 10-year-old population. The remaining 10 per cent accounts for those that would choose not to use personal ICTs, those that are prevented from doing so, such as prisoners, and those who use shared facilities. It includes only people over age 10 to accommodate for data protection measures and privacy laws protecting children.

4G or equivalent broadband: Good quality broadband internet is defined as an average download speed of at least 10 Mbps and as technology neutral (meaning that data may be transmitted via cable, fibre, satellite, radio or other technologies) as possible to ensure internet access is meaningful and has the potential to be transformational. This means 4G is used as the proxy for mobile broadband, and fixed broadband applied where most relevant, such as communities accessing the internet through Wi-Fi hotspots powered through fibre-optic.

Meaningful connectivity: See A4AI’s definition for meaningful connectivity and its call to action to revise how internet connectivity is redefined. Annex C provides an overview of the different connectivity technologies available and their impact on user experience.

While this analysis does not account for country-specific differences, it provides a regional insight into the magnitude of the economic impact that universal connectivity could bring.

Growth in GDP from increased connectivity only, cumulative by developing country region. Total: $8.7 trillion

Chapter 7

We only model the impact of an increase in mobile broadband penetration, excluding the additional impact of an increase in fixed broadband use. This is to offer a more realistic, albeit conservative, estimate of the impact of closing the digital divide – based on reaching universal internet access that would predominantly be driven by providing users access to 4G, or equivalent, broadband through a compatible device (in most instances, a smartphone).

It is pertinent to note that the economic impact of an increase in mobile broadband for low-income countries is highly significant, becoming less significant as countries’ incomes increase. However, the inverse is true of fixed broadband, where increases in penetration are not statistically significant for low-income countries, but for middle- and especially higher-income countries, the GDP impact increases (see Table 1).

The current mobile broadband penetration rate is far higher than for fixed. In the developing world, there are 65 subscriptions for mobile broadband, compared to 12 fixed-broadband subscriptions for every 100 inhabitants. Even in the developed world, mobile broadband penetration is far higher with 125 subscriptions per 100 inhabitants for mobile broadband, versus 34 subscriptions for fixed. Most people access the internet through a smartphone – 89 per cent of internet users use a smartphone to connect, based on A4AI’s Meaningful Connectivity survey. Of those that use other devices, such as laptops and tablets, only 2.3 per cent of those same respondents use this as their only means of connecting to the internet.

Mobile broadband will continue to be the primary route for new internet to get online. For developing countries, an increase in mobile broadband penetration is not only more impactful, it is also where the bulk of investment will likely go (despite the investment case for closing the digital divide, as detailed in the next chapter, being technology agnostic). Hence we only model the impact of an increase in mobile broadband penetration on economic growth, and thus the economic benefits outlined above are conservative.

Comparing Costs and Benefits

The economic benefits of reaching universal internet access far outweigh the investment costs at a macro-regional level:

Economic benefit versus cost of achieving universal internet access, by region (costs excl. devices)

Note: Does not include $18 billion cost for device access. This is not included as we do not have regional data available.

Source: TBI analysis based on World Bank and ITU data. Regions based on World Bank classifications.

Not only do the econometric benefits greatly outweigh the costs – by a magnitude of over 30 times in the case of East Asia and the Pacific – but these benefits are likely to be underplayed. There are three reasons why. First, while taking into account the macro productivity gains of internet access, these estimates do not include the wider socioeconomic benefits from universal internet access such as: poverty alleviation, improved health and education outcomes, potential redress of gender inequalities through financial inclusion, for example, and improvements across other SDG dimensions.

Second, we only account for the economic impact of an increase in mobile broadband penetration, but the investment model for reaching universal internet access is technology agnostic. It is likely that this will mostly be through 4G, but in some instances it will be through fixed broadband, and it does not account for whichever subscription or devices a user might choose to access the internet. Moreover, existing insights highlighted above illustrate that almost all internet users access the internet through mobile, yet some of may also do so through other devices that are more likely to connect via fixed broadband. Thus, the impact and benefits of an increase in fixed broadband use as a result of overall achievements in universal internet access are not modelled or accounted for in this case.

Third, we used projected population growth figures for 2030. Most of the benefits are likely to accrue after this date, depending on the sequencing of investments, and population growth after 2030 will impact the overall benefits of universal internet access. Population size in developing countries is likely to continue growing after 2030, further amplifying the benefits of universal internet access. Thus, the estimate provided is modest.

Scenarios

The sequencing of these investments is a policy decision and the benefits are likely to accrue over an uncertain time period. We investigated a range of different scenarios for timing and discount rates by region and in every scenario the benefits outweighed the costs.

Net present value (NPV) evaluations of investments and benefits were undertaken by region. The various scenarios included an estimation of the NPV by region if:

The benefits and the costs were spread evenly over the course of the project.

The benefits were only accrued in the last seven years of the project.

The investments were front-loaded, and the benefits accrued only in the last seven years.

The investments were front-loaded and only 70 per cent of the benefits were accrued over the last seven years.

The investments are back-ended and only 70 per cent of the benefits are accrued over the last seven years.

We stress-tested these against the average World Bank discount rates for infrastructure investments (10 to 12 per cent),[_] as well as a more commercially viable rate of 20 per cent (as advised by industry experts to be reflective of more risky country investments, such as in Africa).

The NPV of investment in universal internet access was positive in all scenarios for all regions. Further analysis can be found in Annex B.

Chapter 8

Why, if the benefits of investment outweigh the costs so significantly, is investment not happening at the scale necessary to close the divide by 2030? Several market failures are to blame.

First, for both telecommunication companies (telcos) and device manufacturers, the incentives to invest are focused on the most lucrative areas of the market. For infrastructure investments, telcos can drive stronger profits – and demonstrate stronger investment metrics to shareholders– by upgrading 4G to 5G than they can for updating 2G, or 3G networks to 4G. Moreover, telcos will usually be incentivised to prioritise investment in more profitable areas (4G to 5G) than low profitability ones, even though upgrading 2G to 3G, or 4G, would increase their revenue streams. Greenfield investments to bring coverage to the unconnected (such as rural, less well-inhabited or less prosperous areas) are often commercially unviable for many telcos.

Similarly for device manufacturers, it is more profitable to develop the next-generation smartphone for which there is high demand than it is to make a cheaper 4G device – for which demand may need to be stimulated. Consequently, unlike other forms of technology, the price of entry-level internet devices has remained stable. Although there are some signs that the market for cheaper devices is increasing in some regions, as seen in Africa from 2018 to 2019 (driven by device manufacturers tailoring their business models to these markets for the first time), often these basic smartphones remain unaffordable for the majority of people in these markets, and it is therefore commercially unviable for many device manufacturers to expand into these regions.

This market failure is the result of a mismatch between those who would benefit from universal internet access and those who, in the current market, would incur the costs. While the benefits of universal internet access will primarily be experienced by citizens and, consequently, the wider electorate, government and the broader national economy, investment in connectivity is shouldered predominantly by the telecoms sector alone.

Second, some industry experts indicate that telcos would expand 4G coverage if the demand existed but that the challenge is predominantly affordability and relevance, rather than a lack of coverage. Many are not accessing the 3G networks that already exist in their area– as indicated previously in Figure 1. The investment necessary to convert a 2G or 3G cell tower into a 4G one is marginal, but the demand is not yet there to justify the investment.

Third, ICT markets in developing countries can be uncompetitive or even closed, making network investment challenging. An estimated 260 million people have only one choice of major mobile network operator, while 589 million people live in countries where a lack of competition keeps prices high.[_] A4AI also notes that progress on market competition is stalling and a lack of transparency on licensing requirements makes entry into new markets challenging. Furthermore, inflated spectrum prices or delays to spectrum allocation – often considered cash cows for governments – stifle competition, hinder infrastructure investment and, ultimately, inflate the cost of data for consumers. Inordinately high levels of taxation in the ICT sector can dissuade new entrants or even force existing market players out. For many governments in developing countries, telco revenues can be one of the most lucrative and reliable income streams available, which makes changing ICT regulation even more challenging.

Fourth, and finally, the investment market for 4G and equivalent technologies may not be fit for purpose. When telcos make significant infrastructure investments, such as laying fibre-optic cables or installing a new tower, they (and their shareholders) currently expect returns on that investment within five-year horizons. This is unfeasible for greenfield investments in unconnected areas where demand is not yet proven and is unlikely to happen in lower-income markets where telcos must wait longer to profit from increased data usage. In these markets, the returns from increased broadband coverage will thus be more meaningful for the wider economy and government treasury.

The private sector has already seen the potential that increased internet access represents and, over the last ten years, investment in narrowing the digital gap has followed. While some companies are aligning investment initiatives with their broader market strategy, others are making considerable efforts to frame their projects within a sustainability approach; Google’s Next Billion Users and Facebook’s Connectivity are two examples of such initiatives. US technology companies including Google, Facebook, Microsoft, Amazon and SpaceX are focusing on expanding network and internet connectivity and are testing innovations and research projects to provide alternatives to traditional infrastructure for remote and underserved areas.

Reliance Jio, an Indian telecommunications company, has brought the internet to more than 400 million people in India and has one of the cheapest data tariffs in the world. It offers plans that dropped the average cost per gigabyte of data to less than $0.10. Its collaboration with KaiOS also helped in significantly lowering the cost of smartphones. Jio has also developed the world’s first 4G smart feature phone with ability to support multiple Indian languages. In addition to developing local language tools and locally relevant content, Jio has enlisted community leaders to train and educate a new group of users.

Telenor – a Norwegian telco with a massive presence in Pakistan, Myanmar and Bangladesh – has been addressing the digital divide in these frontier markets by taking into account the countries’ socioeconomic context.

The influence of the Chinese technology giants on the African market has already been discussed. Some Chinese companies dominate on market penetration, mobile handsets or network connectivity, partly thanks to the Chinese government’s financial support as part of its Belt and Road Initiative. However, these private-sector investments have not yet been extensive enough to deliver universal access at a global scale.

Private investment has also driven expansion of internet technologies. Despite market failures to expand internet access to the many, most governments and private investors still believe that 4G and equivalent network expansion should be led by the private sector. Most multilateral development banks (MDBs) such as the World Bank put much of their efforts into helping countries create the right enabling environment for private investment to step in. The ITU and A4AI, in their Connecting Humanity, 2020 report, expect the private sector to contribute 75 per cent of the $382 billion infrastructure investment necessary to achieve universal internet coverage, drawing on the World Bank Group’s Maximising Finance for Development (MFD) approach. A key question is therefore how to shore up private investment to reach universal internet access by 2030.

Chapter 9

The economic case – not to mention the moral case – for closing the digital divide is unequivocal. The potentially greater challenge, then, is to identify realistic implementation strategies for universal coverage by 2030.

Here we identify key policies that: a) begin to address the market failure; and b) provide a more hospitable environment for the private sector to bridge the investment gap.

Stimulating Demand

Demand for internet access must first be stimulated to build the case for private-sector investment in 4G coverage (or equivalent). This should be done through three routes:

Subsidies and loans to increase access to a smartphone device.

Public investment in developing the digital skills necessary to access the internet.

Public investment to shape the content on the internet to make it relevant to all.

The donor community and national governments both have a role to play in stimulating demand through public investment.

What Should Donors and the Wider Global Community Do?

Mobilise approximately $58 billion of public funds to stimulate demand in 4G and equivalent broadband technologies between now and 2030.

$18 billion for supporting universal access to a smartphone by 2030. Around 56 per cent of this investment would be focused on subsidies to support smartphone access for the extreme poor, while the remaining 44 per cent would be used to underwrite loans made by telcos that are designed to help lower-income consumers purchase a smartphone through an affordable repayment plan.

$40 billion for building the digital skills necessary and the relevant content to make access to the internet meaningful for all. This figure is derived by the ITU and A4AI as part of their Connecting Humanity investment analysis, based on a nominal cost per user to improve the skills and content for internet access.

This figure is indicative of the scale of investment needed to reach universal internet access by 2030. Further analysis will be necessary to identify existing and planned national-level investments already being made in this area. The investment picture will remain dynamic through to 2030 as more innovative policies and technologies solve digital usage challenges.

Donors should use these funds to encourage governments to implement national strategies for increasing device access and expanding digital skills and relevant content. This could involve requiring governments to meet certain targets before they can access funds to drive demand in 4G or equivalent broadband. It would also involve providing guidance and best-practice insights for addressing these demand challenges.

What Should Governments Do?

Address access to a smartphone device through Universal Service and Access Funds (USAFs). [_] USAFs are often underused and opaque. The donor community should initiate a global review of the current status of these USAFs (similar to A4AI’s assessment in 2018 that $400m across Africa’s USAFs remained unused) to ascertain how much investment can be delivered by national funds and what remains to be committed by the donor community.[_]

Invest in building web literacy. Citizens must learn a basic understanding of the web and web technologies, giving them the confidence and satisfaction to read (how we explore the web) to write (how we build the web) and to participate (how we connect on the web). This can be done through:

National education curricula. Learning by doing will be critical – studies indicate that simply providing digital equipment (e.g., tablets) to children without teacher assistance can stimulate learning alone[_] – and thus digital literacy will be built by children being exposed to, and indeed learning through, use of the internet and digital technology. This will be catalysed once every school is connected to the internet, a target championed by the ITU and UNICEF’s GIGA initiative.

Lifelong learning initiatives focused on building digital skills across specific marginalised groups (e.g., women, farmers). Ring-fenced funding across relevant sector ministries should focus on building digital skills of those in post-formal education through community-based training facilities attached to connected schools.[_]

Invest in making the internet relevant by:

Launching national and local grant-backed competitions to promote development of digital content and software to increase internet access. These could focus on the translation of websites and development of voice-activated programmes in local languages, and building apps to develop basic skills (e.g., literacy and numeracy), advanced skills (e.g., critical thinking) and digital skills more broadly. Apps that serve previously unconnected groups, such as AgTech for smallholders, should also be encouraged.

Leading by example by building out digital public-service delivery alongside increased internet access. Citizens become more web literate by practicing through civic engagement, e.g., accessing social-security payments or health facilities.

Regional Coordination

Public investment alone may not be enough to stimulate the necessary demand for 4G and equivalent broadband technologies. Regional and global coordination will be required for some of the above initiatives to reach scale.

Regional bodies such as the African Union, along with those donors investing to stimulate demand in 4G and equivalent broadband technologies, should drive acquisition of cheap smartphones. This will likely involve engaging with multinational telcos and governments to map the devices gap in each country and bulk order smartphones at a discounted rate from original device manufacturers (ODMs).[_] These smartphones can then be provided either directly to beneficiaries (the extreme poor) through national governments, or purchased by telcos to sell via device-repayment plans targeted at the lowest-income groups.

Regional bodies should also work with telcos and other private-sector actors to reduce the cost of data in developing countries. Across Africa, for example, prices exceed the universal target for affordability (1GB at 2 per cent of monthly income) in the majority of countries. The Smart Africa Alliance, made up of 31 countries, has launched a “bulk capacity purchase project” for data capacities in 2021 and is aiming to reduce the cost of the internet on the continent by 50 per cent. Capacities purchased in bulk on telecommunications infrastructure from connectivity providers will be resold at affordable prices in the member countries of the Smart Africa Alliance. More initiatives of this kind will be transformational in driving down the price of data.

Regulatory Reforms

Regulatory changes will be essential for creating an environment that stimulates private-sector investment in both expanding 4G and equivalent broadband-network infrastructure and driving down the cost of data and devices. Emerging technologies, such as LEO satellites, will push the boundaries of traditional approaches requiring regulation to evolve (see Annex D). Policy amendments can also go some way in addressing the affordability challenges those not currently accessing the internet face.

Again, both national governments and the wider development community have a role to play in opening up ICT markets and stimulating competition in the sector.

Governments Should: